.svg)

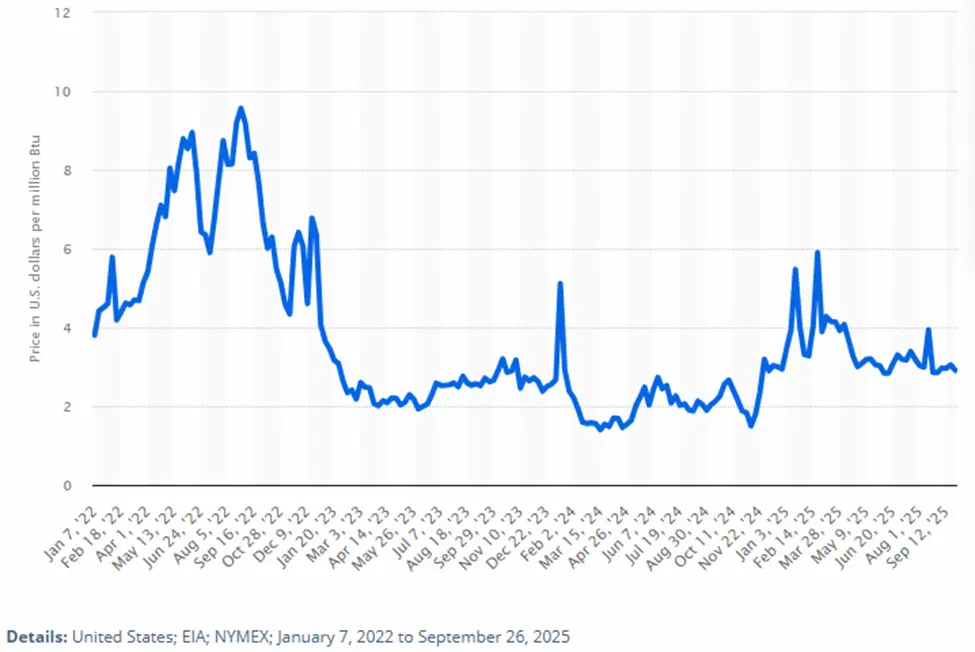

2026 is just around the corner, and with it, come changes to the outlook for natural gas suppliers in the U.S. The EIA’s October 2025 outlook projected that lower 48 marketed production will be near or above 118 Bcf/d in 2026, with the Henry Hub averaging roughly $3.90/MMBtu as storage exits Winter 2025–26 above the five year average. Exports of LNG are forecast to rise from 2025’s 14–15 Bcf/d to 16+ Bcf/d in 2026, as new liquefaction trains go online. Note these volumes refer to liquefied natural gas and are distinct from domestic pipeline gas markets.

Additional reporting at Natural Gas Intel predicts that the lower 48’s storage surplus will “vanish” ahead of the winter. So, the questions facing the LNG sector at the close of 2025 are whether the surplus will hold out, if existing production capacity can meet demand, and can new plants go online quickly enough to mitigate dwindling stores?

Increasing electricity demands from AI and data centers are also reshaping the nation’s gas burn profiles. TC Energy and other midstream operators are now predicting sizeable incremental gas demand from data-center related power generation into 2030. The company is planning cases citing a 45 Bcf/d increase in North American demand by 2035. The increases will be partially driven by tripling LNG exports and rising power sector needs. Analyses by Data Center Dynamics and the International Energy Agency (IEA) concluded that data centers will lift energy generation requirements overall, with natural gas meeting a material share of the load through the next decade.

Upstream Focus: Supply, Basins & Deliverability

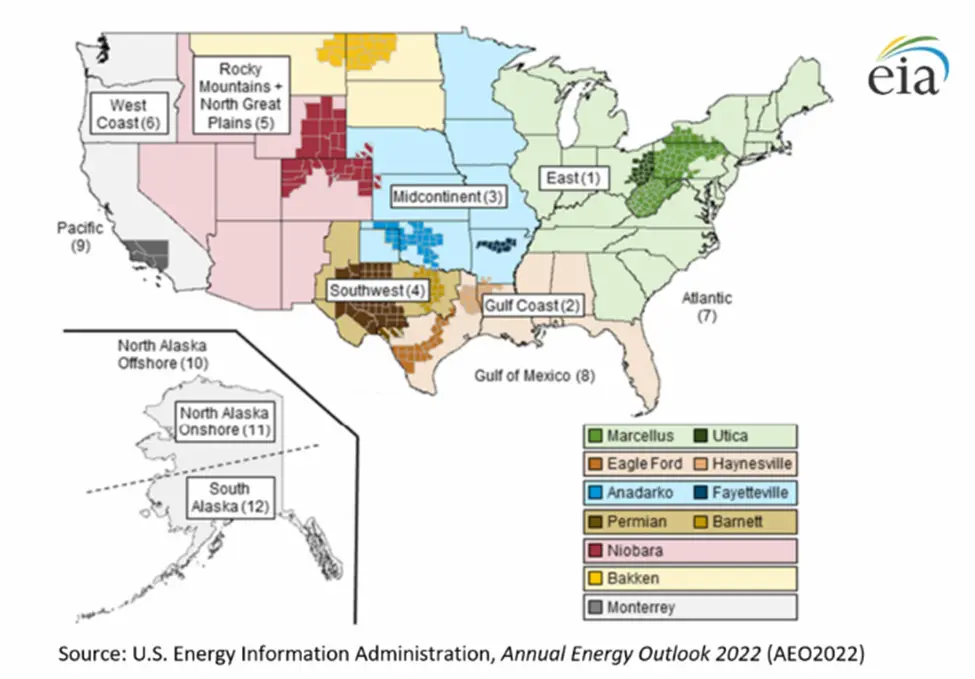

Natural gas production growth is concentrated in Appalachia, the Permian Basin (West Texas and Southeast New Mexico), and The Haynesville (Northeast Texas and Northwest Louisiana), and is largely driven by “North America’s shale revolution.” McKinsey estimates these basins drove roughly three quarters of North American shale natural gas growth in 2014–24. Further gains will hinge on takeaway additions and basis management. In the near term. The EIA expects 2026 output will increase, with Haynesville activity ticking up as prices firm and LNG gas demand continues to expand. Operators are balancing capital discipline with DUC drawdowns to sustain deliverability.

Meanwhile, permitting and access issues continue to limit production rates in the Northeast. While the Mountain Valley Pipeline is now online, new greenfield capacity remains scarce; upstream growth west and south is advantaged where midstream expansions tie directly to Gulf Coast LNG demand.

Midstream Focus: Pipelines, Compression & LNG Linkages

FERC’s docket shows a busy queue of interstate expansions weighted to compression and looping that debottleneck flows into Gulf Coast corridors and Southeast load centers. Pending and recently approved projects add both pipe miles and large blocks of horsepower. The Mississippi Crossing and South System Expansion 4 programs, among others, are lead drivers of that growth.

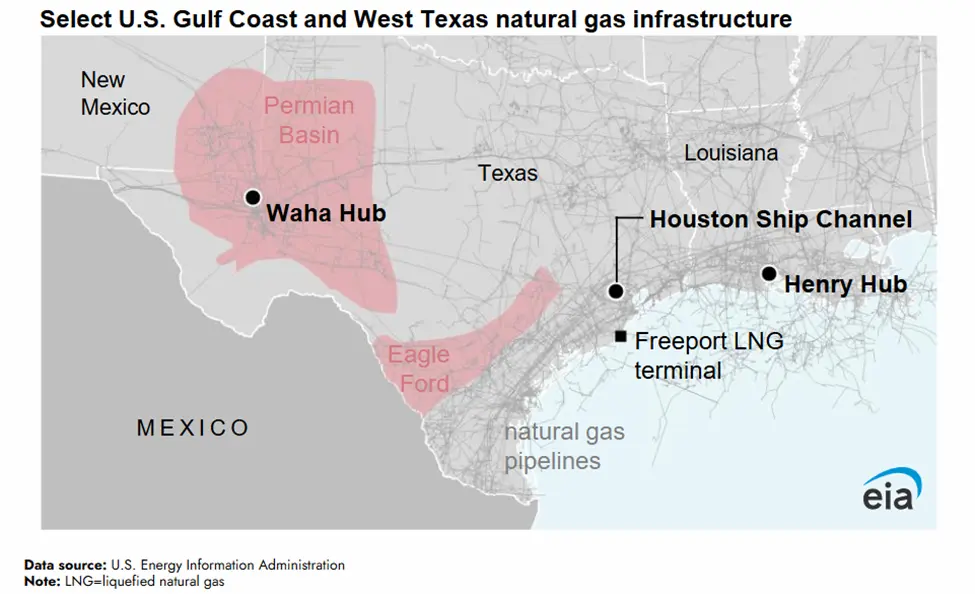

Multiple large scale gas pipelines entering service or nearing FID to align basins with LNG liquefaction along the Texas Louisiana coast are playing a large role in the rosy market outlook. Publications like Pipe Exchange note that most of the 2025 optimism was driven by Permian and Haynesville takeaways to LNG, and project lists include 1.8–3.5 Bcf/d long haul systems slated to go online in late 2025 and throughout 2026. These long-haul projects are pipeline gas assets feeding LNG plants, not LNG terminals themselves.

LNG developers have locked in near record term contracts in 2025, despite higher fees, supporting financing, and new flame ionization detector (FID) requirements. Recent Federal policy shifts lifted an earlier non FTA export pause, and the Department of Energy now shows long term authorizations exceeding 55 Bcf/d, with 28+ Bcf/d in operation or under construction. These figures pertain to liquefied natural gas export capacity, distinct from domestic transmission.

Large midstream operators are signaling consistent commercial outlooks: TC Energy and its peers expect steady project completion through 2028 to serve upsurging LNG and overall power loads, although near term transport volumes will continue fluctuate with price and storage.

Downstream Focus: Power, LDCs & Industrials

The primary swing component in the downstream outlook is power sector burn. The EIA and independent analyses from industry watchers like Marketplace predict some near term variability, but see a structural upside as new load centers come online. Utilities pursuing additional firm gas capacity to support reliability are driving positive market sentiment, although regional constraints may limit gas fired LNG additions without parallel pipeline upgrades.

Local distribution companies (LDCs) and industrials continue to modernize and enact methane reduction programs while evaluating future readiness for low carbon gases. GTI Energy’s NZIP work seeks to provide options that leverage existing distribution and storage assets for renewable gas and hydrogen blends over time. Though material compatibility and safety envelopes still require rigorous validation and testing before this approach can be factored into production/demand.

Practices & Outlook for Transmission & Distribution Technologies

Some natural gas pipeline operators are deploying larger compression and fiber optic distributed acoustic sensing for leak and intrusion detection, in a quest for efficiency, plus advanced inline inspection to reduce methane intensity and O&M costs. Digital and robotic leak detection architectures that merge fiber optics, aerial surveillance, and ML based analytics (AI) are beginning to scale up from initial pilot projects on long haul corridors.

Two parallel issues present regarding transmission & distribution:

- Re-aligning & upgrading capacity to LNG and power hubs. Additional long haul capacity and station upgrades from the Permian and Haynesville to the Gulf will be needed to sustain higher LNG distribution and transmission to serve data center clusters in the Southeast and Mid Atlantic.

- Material and design readiness for a new molecular future. Hydrogen embrittlement risks and CO₂ phase behavior challenge the ongoing efficacy of legacy steel systems. While the short-term focus is on methane service integrity, any hydrogen systems that seek to blend on transmission will require controlled pilot programs, selective materials, and revised safety codes.

Navigating the Current Regulatory Environment

FERC has continued to process certificate applications under NGA Section 7 with updated NEPA procedures. Publicly posted project lists and “priority projects” pages listed by FERC indicate several Gulf Coast the prioritization of expansions linked to LNG. Concurrently, DOE/FERC actions in 2025 shortened timelines for LNG terminal approvals, materially affecting export project schedules.

What Do the Forecasts Mean for 2026 Pipeline Design, Engineering & Construction?

Trends show that commercial construction is skewing toward high horsepower brownfield compression, loops along existing ROWs, and targeted greenfield laterals for LNG, power plants, and industrial load. Stringent methane controls are leading to strict safety protocols and testing during construction, expanded fiber optic monitoring requirements on new pipe, and more utility scale interconnect work near data center nodes.

How GPRS Supports Gas Pipeline Construction, Compressor Stations, and Distribution

GPRS provides 99.8% accurate subsurface utility locating and concrete scanning, provides clearances and post-application confirmations for trenchless path technology, and full 360°, below and aboveground as built mapping to reduce strike risks, clashes, rework, and schedule slip across upstream adjacent gathering builds, interstate compressor expansions, and LDC distribution upgrades. These services directly align with 2025–2028 build patterns documented in FERC and industry outlooks, and support SUE at quality level B.*

- Pipeline and Compressor Projects: Precise locating and 3D utility mapping enable safe HDD/auger bores and compressor station tie ins along congested right-of-ways where new loops and large HP additions dominate project scope. An increasing number of FERC listed projects emphasize station upgrades and parallel loops, so require clash-free alignments and verified clearances to shorten outage windows and commissioning.

- Distribution Systems: For LDC main replacement and pressure reducing systems (PRS) work, GPRS’ GIS ready as builts and ground penetrating radar concrete scanning eliminate most risk from urban digs and compressor station modifications, supporting modernization and methane reduction mandates highlighted in sector research.

- Project Command & Control: At GPRS, we say that “data control = damage control” because when you control the quality, capture, and flow of information for your project, your team can all be on the same page, with the same accurate data they need to make the most informed decisions. That’s why we build SiteMap® (patent pending) our secure, accessible, and fully portable cloud-based GIS platform to house your deliverables from initial utility locate through integrated 360° BIM models, progress capture, walkthroughs and more, all accessible inside Sitemap, with full data portability to any other GIS platform you choose. Every GPRS customer receives complimentary Sitemap Personal access, so you can securely share, print, export, communicate, and collaborate with the data you need to plan, build, and manage, better.

By combining the industry’s highest accuracy locating, mobile mapping, and deliverables that easily export to other GIS and construction management systems, GPRS helps EPCs and operators meet tighter safety, methane, and schedule requirements that accompany LNG linked timelines and data center driven interconnects.

What’s the Bottom Line in LNG for 2026?

Upstream deliverability remains adequate, but just barely. And midstream and downstream infrastructure need to expand and update to keep pace with the two biggest market demand engines: LNG exports and power for digital load growth. The 2025–2029 window will feature compressor station expansions, selective new long haul pipes to the Gulf Coast, and targeted urban distribution modernization, with technology and QA/QC practices focused on safety, methane, and constructability.

What can we help you visualize?

*GPRS is not a surveying company and does not provide subsurface utility engineering surveys. Our highly accurate utility locating & mapping, however, does support QL-B for SUE and can be of use to licensed surveyors to speed results.

Frequently Asked Questions

What is the Henry Hub and how does it work?

The physical Henry Hub is located along the Southeastern U.S. coast in Erath, Louisiana, and is a nexus of nine interstate and four intrastate pipelines and other natural gas infrastructure. The Henry Hub also acts as a baseline for global LNG pricing because it is also the “official delivery spot for NYMEX futures contracts,” per Investopedia. It is owned by Sabine Pipe Line, LLC, and its pricing is based on supply and demand, in contrast to the oil-indexed pricing of Europe.

The pipelines that meet at the Henry Hub include:

Interstate:

- Acadian

- Columbia Gulf Transmission

- Gulf South Pipeline

- Natural Gas Pipeline Company of America (NGPL)

- Sea Robin Pipeline

- Southern Natural Pipeline (Sonat)

- Texas Gas Transmission (Transco)

- Trunkline Pipeline

Intrastate:

- Bridgeline Pipeline

- Jefferson Island Storage & Hub

- Sabine Pipeline

- Louisiana Intrastate Gas (LIG)

Learn more about how GPRS supports compressor station upgrades, right-of-ways, and new pipeline construction.

What Is a Liquification Train and How Does It Work?

A liquification train is a term that refers to a self-contained set of industrial processes and technologies that cool and “shrink” natural gas to liquefy it for storage and shipping. It’s known as a train because each set of equipment and processes are sequential to purify and liquify the gas. Most LNG plants have multiple liquification trains, and onshore base load plants produce an average of 4 million metric tons annually.

There are five main stages in a natural gas liquification train: pretreatment, acid gas removal & dehydration, heavy hydrocarbon removal, liquification/cooling, and storage/transport.

2026 is expected to bring a “mega-LNG wave,” globally and in the U.S. with many high-profile projects either underway or planned. FERC shows 24 major pending pipeline projects as of September, with liquification trains for Corpus Christi Stage 3 and Plaquemines Phase 2 both due online in 2026. Rio Grande LNG (Trains 1-3) and Port Arthur Phase 1 are due to commence operations in 2027-2028. The first train of Golden Pass LNG is expected to be online by the end of 2025, with Train 2 coming online in mid-2026, and Train 3 due near the end of next year.